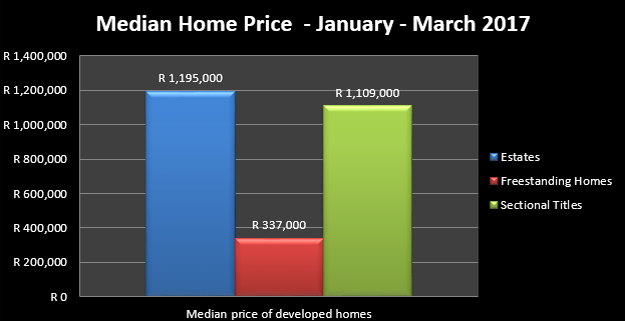

While the thought of owning and letting out property is an appealing financial venture to many, there is more to being a landlord than collecting the rent each month, says Adrian Goslett, Regional Director and CEO of RE/MAX of Southern Africa.

“Depending on the circumstances, owning a rental property can be fairly time consuming and involved, especially if you decide to manage the property yourself,” says Goslett. “It is possible for the endeavour to be financially rewarding, but it is vital to be fully aware of what it entails before taking the leap. Understanding what is involved and doing some research on the matter will put you in the best position to handle whatever may come your way and increase the chance of making it a success.”

Here are five aspects that all potential landlords should think about when considering getting into the property rental business:

1. You are in it for the long haul

Property should be considered a long-term investment - it takes time for property to appreciate in value and build equity. A rental property will likely get to the stage that it is paying for itself, or ideally making a profit – but this will take time. “While possible, it is rare that the rental will cover all the costs from the outset. Whether part of the bond repayment or merely maintenance of the property, it is likely that you will need to carry some of the monthly costs in the beginning. However, the rental amount will increase over time, reducing the amount of money you as the landlord will need to cover. Eventually, it will get to the point where the rental covers all costs, and there is a profit generated. Getting to this tipping point won’t happen overnight, it can be a drawn-out process that requires patience and resolve to see it through,” says Goslett.

2. The bond won’t be the only expense

Consider all the costs involved with owning property, not just the bond. Landlords need to know the numbers. Aspects to take into account include general maintenance, insurance, rates and taxes and possibly the services of an attorney or a professional rental agent. An attorney is a valuable asset when it comes to drawing up lease agreements, as well as providing sound legal advice regarding your rights and responsibilities. There is also the matter of dealing with defaulting tenants should it be necessary. A rental agent will take care of screening and vetting tenants, collecting the monthly rental and general management of the property.

“Provision should be made for the upkeep of the property, along with any other unforeseen circumstances or repairs that require attention. Setting money aside in a contingency fund must form part of a landlord’s monthly budget. Knowing the numbers and budgeting for expenditure will ensure that money is allocated to where it needs to go,” says Goslett.

3. Have a checklist

Having a checklist that includes all items you need to go over when a tenant moves in and again when they move out, will ensure that nothing is overlooked. It will help you to assess the property and ensure that it is in a good condition when handing over the keys. The same checklist can be used when the tenant moves out, to compare the condition of the home to its state before the tenant took occupancy.

Items that should appear on the checklist could include the following:

• Check that the stove is in working order.

• Check all lights and electrical points.

• Ensure the geyser is working correctly.

• Check for any leaks or damp that needs waterproofing.

• Check that the gutters are unclogged and clear of debris.

4. Make sure contracts include all details

All stipulations should be clearly stated upfront in a detailed contract to avoid any future complications or misunderstandings. The more detailed the contract the better, as there is less chance of any ambiguity. If aspects of the tenancy are dealt with in the contract, there will be no areas left open for interpretation. Factors such as acceptable tenant behaviour, breakage costs, preferred method of payment and date that the rental is payable by should be all included in the document.

5. Vetting and selecting the right tenants

The financial success of a rental property is largely determined by tenant selection. Prospective tenants must be carefully vetted before a rental agreement is concluded. If possible, obtain details of the tenant’s previous rental history, reasons they are moving, their place of employment and income. References should be contacted to verify as much of the information as possible. “The tenant vetting process is where the services of a rental agent will be a valuable asset. While discrimination against tenants is illegal, it is not wise to simply accept the first tenant who applys for the property,” advises Goslett.

While not for everyone, owning a rental property can be a vehicle for wealth creation over the long term - the key element to success is to always view property investment with the future in mind.